All Categories

Featured

Table of Contents

[/image][=video]

[/video]

You can underpay or avoid premiums, plus you may be able to change your death benefit.

Money worth, along with possible growth of that value through an equity index account. An alternative to designate component of the cash money value to a fixed rate of interest alternative.

Università Telematica Iul

Policyholders can make a decision the percentage designated to the dealt with and indexed accounts. The worth of the selected index is videotaped at the beginning of the month and compared to the worth at the end of the month. If the index boosts during the month, rate of interest is included to the cash money value.

The resulting rate of interest is added to the cash money worth. Some policies compute the index gains as the sum of the modifications for the duration, while various other policies take a standard of the daily gains for a month.

Indexed Universal Life Insurance Versus Life Insurance Policy

The price is set by the insurer and can be anywhere from 25% to more than 100%. (The insurance company can likewise change the get involved rate over the life time of the policy.) For example, if the gain is 6%, the participation price is 50%, and the current cash worth total is $10,000, $300 is included in the cash worth (6% x 50% x $10,000 = $300).

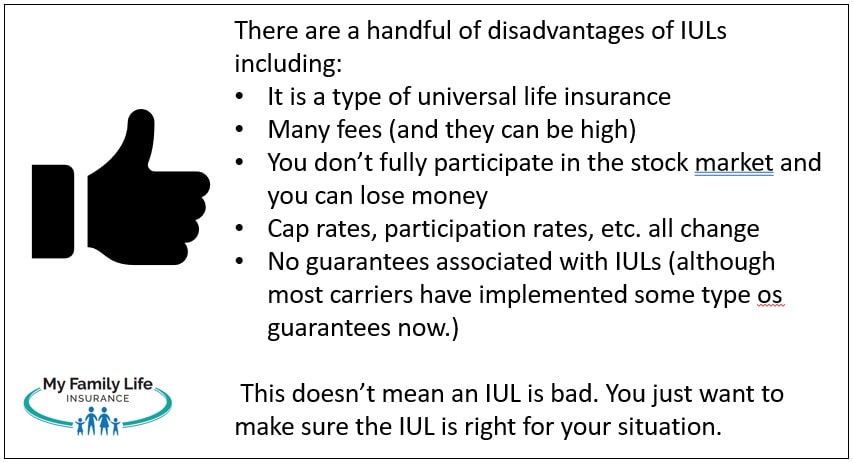

There are a number of advantages and disadvantages to consider prior to buying an IUL policy.: Just like common global life insurance, the insurance policy holder can increase their premiums or reduced them in times of hardship.: Amounts credited to the cash money worth grow tax-deferred. The cash money value can pay the insurance premiums, allowing the insurance policy holder to lower or stop making out-of-pocket costs payments.

Numerous IUL plans have a later maturity date than various other sorts of global life policies, with some finishing when the insured reaches age 121 or even more. If the insured is still alive at that time, plans pay out the survivor benefit (however not normally the money value) and the proceeds might be taxable.

What Is An Indexed Universal Life Insurance Policy

: Smaller sized policy face values don't offer much benefit over normal UL insurance policy policies.: If the index drops, no interest is credited to the cash value. (Some plans provide a low ensured price over a longer duration.) Other investment vehicles make use of market indexes as a benchmark for efficiency.

With IUL, the objective is to make money from higher activities in the index.: Since the insurer only gets options in an index, you're not directly invested in stocks, so you do not profit when firms pay dividends to shareholders.: Insurers charge fees for managing your money, which can drain pipes money worth.

For many people, no, IUL isn't better than a 401(k) in terms of conserving for retirement. A lot of IULs are best for high-net-worth people seeking ways to reduce their gross income or those that have maxed out their other retired life alternatives. For everyone else, a 401(k) is a far better financial investment vehicle since it doesn't bring the high fees and premiums of an IUL, plus there is no cap on the quantity you may make (unlike with an IUL policy).

While you may not lose any money in the account if the index goes down, you will not earn rate of interest. If the market turns bullish, the incomes on your IUL will certainly not be as high as a common financial investment account. The high expense of premiums and costs makes IULs pricey and significantly much less budget-friendly than term life.

Indexed universal life (IUL) insurance policy uses cash money value plus a death benefit. The cash in the cash worth account can make interest with tracking an equity index, and with some often designated to a fixed-rate account. Nonetheless, Indexed global life plans cap just how much cash you can build up (typically at less than 100%) and they are based on a potentially unpredictable equity index.

Iul Master

A 401(k) is a better option for that function due to the fact that it does not lug the high fees and costs of an IUL policy, plus there is no cap on the amount you may make when spent. Many IUL plans are best for high-net-worth people seeking to decrease their gross income. Investopedia does not supply tax obligation, investment, or monetary solutions and suggestions.

Your present browser may restrict that experience. You might be using an old browser that's in need of support, or setups within your internet browser that are not compatible with our site.

Your existing browser: Detecting ...

When your selected index picked value, worth too does as well policy's plan value. Your IUL cash money worth will additionally have a minimal passion price that it will certainly always earn, regardless of market efficiency. An IUL policy functions the exact same means as a traditional global life plan, with the exemption of just how its cash value earns interest.

Index Universal Life

If you're thinking about getting an indexed global life plan, initial speak to a financial expert that can clarify the subtleties and provide you an accurate photo of the actual potential of an IUL plan. See to it you comprehend how the insurer will determine your interest rate, revenues cap, and charges that could be analyzed.

Part of your premiums covers the policy price, while the remainder goes into the cash worth account, which can expand based on market efficiency. While IULs might appear attractive, they generally feature high charges and inflexible terms and are completely inappropriate for several capitalists. They can generate rate of interest yet additionally have the prospective to lose money.

Here are some factors that you must think about when figuring out whether a IUL policy was right for you:: IULs are complicated monetary items. Make certain your broker fully explained how they function, including the costs, financial investment dangers, and cost frameworks. There are more affordable options available if a survivor benefit is being looked for by a capitalist.

Università Telematica Degli Studi Iul

These can substantially reduce your returns. If your Broker stopped working to give a thorough explanation of the costs for the policy this can be a red flag. Be aware of surrender fees if you make a decision to terminate the plan early.: The investment element of a IUL undergoes market changes and have a cap on returns (definition that the insurance company obtains the benefit of outstanding market performance and the capitalist's gains are covered).

: Ensure you were told concerning and are able to pay enough costs to maintain the plan in force. It is important to thoroughly research and recognize the terms, costs, and potential dangers of an IUL plan.

Standard development financial investments can typically be coupled with much more affordable insurance coverage alternatives if a survivor benefit is important to an investor. IULs are excluded from federal law under the Dodd-Frank Act, implying they are not managed by the united state Securities and Exchange Commission (SEC) like supplies and alternatives. Insurance policy representatives offering IULs are only required to be accredited by the state, not to go through the exact same strenuous training as stockbrokers.

{kind=link}

Table of Contents

Latest Posts

Index Universal Life Insurance Policy

Iscte Iul Fenix

Iul Insurance Meaning

More

Latest Posts

Index Universal Life Insurance Policy

Iscte Iul Fenix

Iul Insurance Meaning